Yes, personal loans can be included in bankruptcy in California, and they are usually dischargeable. This includes personal loans from banks, credit unions, friends, family, or employers. Unsecured personal loans, which are loans not backed by collateral, are eligible for discharge in both Chapter 7 and Chapter 13 bankruptcies.

Filing bankruptcy in California involves understanding the types of debt dischargeable, assets and exemptions, eligibility criteria, credit impact, costs, legal procedures, and the role of a bankruptcy lawyer in guiding individuals through the process.

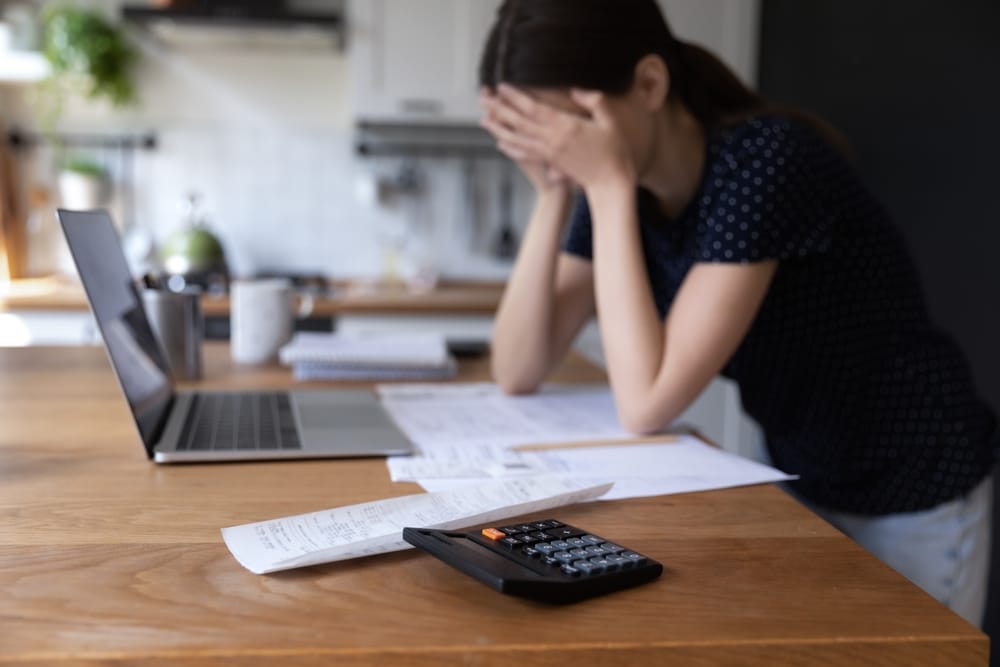

Continue reading “Can Personal Loans Be Included in Bankruptcy in California?”